GetBusy PLC #GETB $GETB.L

SaaSpocalypse survivor? 1.6x EV/ARR with incentive to return £150m to shareholders (Market Cap £35m)

I have broken this write up into two parts; the initial is the catchy investment opportunity overview which we all love, and the second part (if you still care by then) goes deeper into the business.

Part One

Key Stats

Enterprise Value: £35.2m

Current Share Price: 70p

FY25 ARR: £22.6m

FY25 EV/ARR: 1.6x

Opportunity

GetBusy is a SaaS company with 97% recurring revenue. GetBusy has two SaaS products, SmartVault (US based accountancy productivity and document management software) and Workiro (document management and compliance platform in the ERP market).

I believe we have two ‘outs’ as shareholders:

The sale of SmartVault the US based accounting software company which has $15.6m in ARR. Management are expecting a 10x EV/ARR multiple which would generate $150m in capital distributions. Although this does seem lofty, management are incentivised to distribute cash to shareholders by 2030. The incentive kicks in above £70m up to £150m of cash distributed by 2030. If these conditions are met the total incentive to the CEO and CFO will be between £8.6m and £32.7m depending on the amount of cash distributed. This will reward us handsomely with after incentive fees returns between 74% and 233% based on current share price. On top of all of this we will still have Workiro left in the business, which although is struggling slightly is profitable and cash flow generative.

No sale of either SaaS product but both are run for cash and not for soley growing ARR for a sale. Management have previously stated in the past they could reach steady state EBITDA margins of 30%. GetBusy has no working capital needs and therefore it doesn’t need additional cash to grow. There is operating leverage within SmartVault and this should inflect profitability in 2026. Workiro is profitable and will hopefully return to growth this year. Option 1 would be much more preferable but option 2 provides a realistic downside protection scenario as this sticky business can through off cash if investment spending is suppressed.

Valuation

The valuation is based on my two ‘outs’ above. Valuing the business based on the steady state method is difficult, as the business has not proven an ability to generate profits, as per its design but I believe based on its operating leverage and the use of AI to streamline costs, it could reach 25% operating margins by 2030.

Distribution Incentives (Bull): The bull thesis relies on the distribution incentives met of between £70-£150m cash distribution by FY30, this would give a fair value of 121p-231p (74%-233% upside). This valuation also assigns no value to the remaining Workiro product, which has significant value.

Steady state (Base): Based on reaching 25% operating margins by FY30 with low revenue growth, we get to a fair value of 101p (45% upside).

This gives a weighted average fair value of 117p (70% upside).

There is additional upside not mentioned in my model. This is the scenario that a cash distribution of higher than £150m is achieved through a higher sale of SmartVault than expected. Given the current M&A landscape and narrative of SaaS I think its best to not model this.

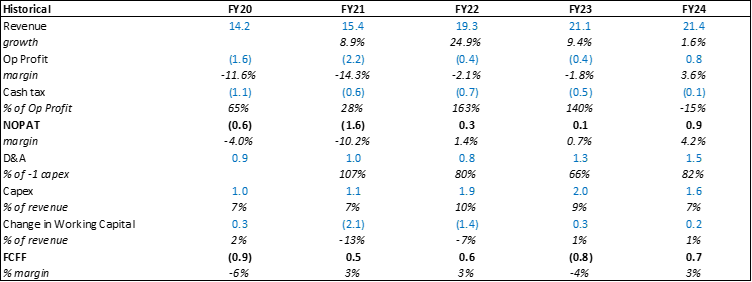

Historical Financials

Revenue has grown at a impressive CAGR of 10.8%, this is mainly due to the strong ARR growth of SmartVault. The slowdown in growth is caused by the combination of Workiro and Virtual Cabinet, which has ultimately led to some churn and a slowdown in growth in the virtual cabinet ARR. Similar to the Amazon model, GetBusy has remained unprofitable but continued to grow due to being cash flow neutral. This is due to working capital being a source of finance rather than a drain due to being paid in advance for subscriptions. This has meant that since going public GetBusy hasn’t had to raise any capital despite being continuously unprofitable.

Risks/What to Watch Out for

AI: The AI threat is definitely real but is it only a threat or is it also an opportunity. Will AI replace every software provider, and be replaced by internal agents? I suspect not. I can see a world where agents are used inside each software provider, this means they will still need a subscription to access. GetBusy’s solutions also has an advantage over other SaaS products as the documents stored and managed need to be kept confidential and therefore there is a compliance/regulation risk with the files stored on these platforms. Accountants are notorious for being cautious and therefore I cannot envisage jeopardise security of documents by switching to a AI tool just to save a few $$.

Workiro: Management have spent a considerable amount of time and capital developing this ERP product, there is a risk that this was a waste if Workiro doesn’t promote ARR growth. This product has been combined with the existing profitable product Virtual Cabinet, but the results are yet to show. ARR growth has slowed due to Virtual Cabinet legacy customers churning due to the being switched to the Workiro platform and while Workiro has grown, it is exposed to longer sales cycles which means gaining customers takes longer but also once customers are won, it will result in higher net retention.

Part 2

Overview

GetBusy PLC was formed in 2017 as part of a spin out from Reckon Limited (ASX:RKN), Reckon aimed to focus on its domestic activities and spun out the document manage division to allow it pursue its own independent growth strategy. Key personnel of the companies are still interlinked as Clive Rabie is the largest shareholder of both and on the board of both companies and his son Daniel is CEO of Getbusy but was previously COO of Reckon. GetBusy is a software group providing document management and client portal/workflow tools used predominantly by professional services firms (e.g. accounting and advisory practices).

Divisions

SmartVault (c.53% of Revenue)

Provider of cloud document management and client portal software servicing US accountants. SmartVault provides support to the entire tax prep workflow for accountants. Tax preparation represents 85% of SmartVaults ARR. Tax preparation clients are particularly attractive as they have higher customer lifetime value and lower churn making the return on customer acquisition far better. The remaining revenue comes from other accounting-based services, which is seeing strong growth due to SmartVaults new unlimited plan. SmartVault is tech stake agnostic and has deep integration with large software firms such as Intuit, Thomson Reuters being there leading cloud document provider. Through this unique resuable integration blueprint, SmartVault provides coverage to almost all tax professionals in the US.

Workiro (c.47% of Revenue)

Workiro has been merged with GetBusy’s document storage product Virtual Cabinet product and now they collectively, serve enterprise customers in the professional and financial services sector, through Workiro integration into ERP systems. Workiro has initially focused on its deep integration with Oracle NetSuite application which provides access to their 41,000 enterprise customers but also has a long-term focus on the broader cloud ERP market. Workiro customers are based in the UK, Australia and New Zealand, as per the connections to the previous owner Reckon. The goal currently for Workiro is to build run rate of new business for the ERP market while also migrating customers from Virtual Cabinet. GetBusy has developed automation for migrating these customers so that should reduce the churn of VC customers as they are migrating. Sales cycles for ERP tend to be long and exposed to sudden delays, although lifetime value in ERP is very high with high sale price and net revenue retention making it an attractive industry.

Capital Allocation

Capital allocation has mainly been spent on internal development costs such as Workiro, which will start to decline going forward as Workiro matures.

A small acquisition was made in 2024 on SmartPath a pricing and revenue optimisation tool which was integration into SmartVault. Terms of the deal were: initial cash payment of US$250,000 and a further cash amount will be payable in 2027 and increases linearly from 30% of Attributable ARR if Attributable ARR is equal to $1,000,000, to 50% of Attributable ARR if Attributable ARR is $2,000,000 or higher. The Contingent Consideration is capped at $2,000,000 and is payable in three equal quarterly instalments starting on 31 March 2027.

Moat and Durability

Unique Deep Integration

Due to being tech stack agnostic, GetBusy can integrate seamlessly into larger software providers.

This integration is a dual benefit to both the large software provider such as Intuit and Net Suite as their product offering improves, lowering customer churn at the same time allows GetBusy to grow its customer base leveraging these larger partners.

At a certain scale of course, Intuit and Net Suite would begin developing their own offering or simply acquire SmartVault or Workiro if they they hit a meaningful size.

Sticky Demand

GetBusy has churn rates of 0.8%, which outlines how sticky the demand for these products is.

Once a business begins using the GetBusy products it becomes extremely difficult to switch providers as staff will have to be retrained and familiarity of features will have to be developed again.

Management Quality

Chair: Miles Jakeman

Appointed Chair in 2017, he was the co founder of Citadel Group Limited which sold in 2020 for over £284m.

CEO: Daniel Rabie

Appointed in 2017, he was the COO of Reckon Limited and led the demerger of GetBusy.

CFO: Paul Haworth

Appointed in 2018, he spent a decade working with Deloitte M&A and has since had finance roles with listed tech manufactures.

Insider Ownership (incl vested options)

Clive Rabie (NED): 23.6%

Daniel Rabie (CEO): 12.4%

Paul Haworth (CFO): 2.6%

Insider Purchases in last 24 months

Clive Rabie: £2.1m, average share price 80p- Annual salary: £41k

Daniel Rabie: £1.4m, average share price 71p- Annual salary: £265k

Paul Haworth: £22k, average share price 61p- Annual salary: £212k

Nice piece, fully agree. Two comments though, the CEO is Daniel Rabie and SmartVault is strongly using AI technology in their tool.